The interest rate hikes set by the ECB are having a tangible impact on the pockets of Italian households, so much so that one percentage point of wages in Italy would be eroded due to the hikes. This was noted in an analysis by Fabi, according to which the share of instalments in disposable income rose from 9.50 per cent in 2019 to 10.55 per cent last March and, given subsequent increases in the cost of money, this percentage is set to rise. The report also highlights which geographical areas suffer the most.

The effects of rising interest rates

In an environment already stressed by inflation and rising utility bills, Italian households also have to cope with rising interest rates. The latest is that of Thursday 27 July from the European Central Bank (at 4.25 percent). The situation resulting from the analysis of rates per mortgage size class with respect to the end of 2021 and 2022 is almost comparable to a financial shock for those with variable-rate mortgages or for those who have yet to buy a house.

In detail, growth averaged 240 basis points over the past year, with growth rates of over 4.5 percent in some areas of Italy. As of March 2023, for mortgages up to €125,000, the average rate on total loans in Italy rose to 4.47%. Mortgages up to €250,000 are at 4.09% and, finally, at 3.74% for amounts above €250,000.

To give an exact idea of the context, suffice it to say that at the end of 2021, Italian households were paying an average rate of 1.49% for loans over €250,000, 1.71% for those between €125,000 and 250,000, and 1.87% for smaller loans.

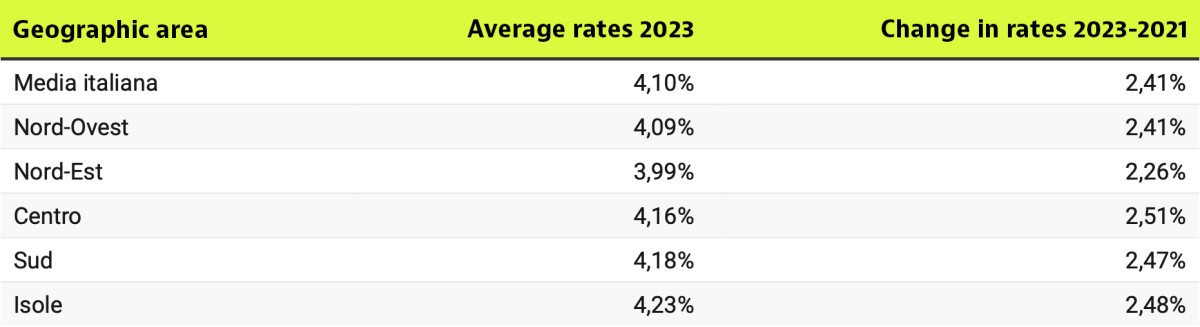

The impact of rising rates by region

But the rise in interest rates is having different effects in different geographical areas. In Italy, there are differences in the amount of a mortgage instalment. In the Islands, the average interest rate is 4.23% and in the Mezzogiorno it is 4.18%, compared to the national average of 4.10%.

The northern regions have more favourable conditions than the rest of Italy for those who need access to a mortgage: the interest rate is 4.09% in the North West (Liguria, Lombardy, Piedmont and Valle d'Aosta) and 3.99% in the North East (Emilia-Romagna, Friuli-Venezia Giulia, Trentino-Alto Adige and Veneto).

The Centre (Latium, Marche, Tuscany and Umbria) saw the most significant increases over the last two years with a spread of 251 points. Some risk factors, which are greater in the south and on the islands, weigh heavily.

The impact of rising mortgage rates

Compared to financing conditions at the end of 2021, the households most affected by rate hikes are those in the southern and central areas of the country, where the cost of money has increased the most. In detail, central Italy is the geographical area with the largest increase: +266 basis points for loans up to €125,000, +246 basis points for loans up to €250,000 and +241 basis points for loans above that amount.

The situation was similar for households in the South, where the smallest differential was recorded only in the category of mortgages up to €250,000, with a differential of 242 basis points, while the widest differential was recorded in the category of mortgages up to €125,000, with 256 basis points, and in the category referring to mortgages up to and over €250,000 the differential was 243 basis points.

In the North-East, on the other hand, the effects of the rise in the cost of money were more limited than in the rest of the country, with a rate differential that came close to 250 basis points for the amount over 250 thousand euro only, while for the other categories of mortgages the differential stood at between 222 (up to 125 thousand euro) and 259 (up to 250 thousand euro) basis points.

Ideas for renovating your home in Italy: tips and inspirations for every need

Buying a home in Italy and renovating it to suit your family's needs is a decision that should never be taken lightly. It’s all too easy to go from feeling overwhelmed to achieving complete satisfaction. This is because navigating the right approach to managing the renovation process without losing your sanity can be challenging. In this guide, we’ll offer simple ideas for renovating your home, breaking down each step you can take to turn your house into the home of your dreams.

How much money do you need to live comfortably in Italy?

Have you ever dreamed of settling down in the picturesque Tuscan countryside? Maybe you’re considering a career change with some of Milan or Rome’s top companies? Or perhaps you just want to spend your days sipping espresso and strolling through the ancient streets of Rome.

The Italian cities with the worst air quality according to Legambiente

The year 2030 is fast approaching, marking a significant shift in environmental sustainability within EU member states. Yet, according to Legambiente, there is still much to be done in Italy. The Mal'Aria 2025 report lists the worst Italian cities for air quality, identifying 25 cities that exceeded the legal limits for PM10 over the past 12 months. Here’s the list.

Flight bonus for Sicily and Sardinia in 2025: who Is eligible?

2025 brings good news for residents of Sicily and Sardinia, who will receive financial support to counter rising flight costs. In both regions, this bonus is becoming a permanent measure and includes a refund that varies depending on the region of origin and specific eligibility criteria. Let’s explore the details of this initiative and all the updates for the new year.

Do solar panels work in winter?

Will solar panels work in winter? This recurring question not only has an answer but is also accompanied by a series of tips to improve the efficiency of photovoltaic technology during the winter months. Experts from ENEA (Italy's National Agency for New Technologies, Energy and Sustainable Economic Development) have released a statement detailing various measures and good practices to adopt during the coldest season to maximise the performance of photovoltaic systems. Let’s find out more.

Tax incentives for foreign buyers in Italy

Italy has long been a dream destination for individuals seeking a blend of culture, cuisine, and scenic beauty. Beyond its lifestyle appeal, Italy offers a range of tax incentives for foreign buyers, making it an increasingly attractive location for international property investors. These incentives are particularly appealing to high-net-worth individuals and expatriates, offering substantial tax benefits and regional advantages.