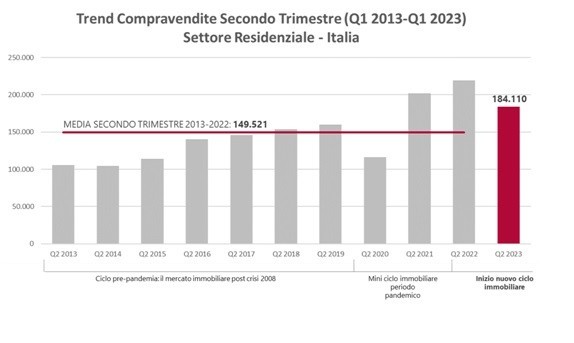

The slowdown in real estate sales is confirmed in the second quarter of 2023. According to data from Agenzia delle Entrate, reworked by Gabetti's Studies Office, compared to the average number of purchases and sales over the last decade of 149,521, Q2 2023 with 184,110 still stands at a good level of purchases and sales, despite the rise in interest rates. However, a drop of 16% compared to the same period last year is evident.

Real estate sales city by city

Looking at real estate sales in the top eight Italian cities, the year-on-year change in the second quarter of 2023 is negative by 16.4%. The trends, when compared to the same quarter of 2022, are down for all cities: Bologna-22.8%, Milan-17.1%, Rome-21.5%, Florence-15.6%, Turin-10.8%, Naples-5.3%, Genoa-14.4%, Palermo-4.9%. The biggest setbacks are still the cities that saw the greatest growth in listings in 2022, such as Milan and Bologna, and those that had achieved an elevated level of sales in the second quarter, such as Genoa. Buying and selling declined more in capital cities (-17.2%) than in non-capital cities (-15.4%).

Real estate purchases and sales in the last ten years

Looking at the second quarter trend of the last 10 years, however, the picture changes significantly. Compared to the last decade's average of 149,521 NTNs, Q2 2023 with 184,110 NTNs is up +23% and ranks as the third best second quarter in the last 10 years, right after the record quarters of 2021 and 2022, which were the offspring of the post-lockdown flare-up in the residential market. Bearing in mind that the count of the last ten years includes the post-subprime mortgage crisis years, in which the real estate market had come to an abrupt halt also due to very high mortgage rates.

Trends in property sales, some forecasts

In light of these data, the macroeconomic and geopolitical dynamics accompanying 2023 seem to confirm the end of the pandemic 2020-2022 mini real estate cycle and the beginning of a new 'normalised' cycle. The start of this new cycle, at least for 2023 and the first half of 2024, will mostly be characterised by an interest rate level that is no longer at historic lows as it was between 2017 and 2021. The disbursement volume of mortgages for home purchase recorded a decrease of 26% between Q1 2023 and Q1 2022.

However, in the light of falling inflation, which from its peak of 11% in December 2022 is expected to settle at around 5% by the end of the year, thus gaining 6 percentage points, it is plausible to assume that the ECB’s tightening of interest rates will ease and already in 2024 interest rates on home loans could be between 2.5% and 3%. This means that a large proportion of mortgage applicants, who currently exceed the bankable parameter of the instalment-income ratio and remain de facto excluded, will be able to obtain a mortgage.

Finally, although the market’s distress in Q2 2023 is evident, comparing it with Q2 2019 (the best first quarter of the pre-pandemic real estate cycle not characterised by the euphoria-anomaly of the years 2021-2022) yields a not so alarming picture. In fact, comparing the trend change between these two quarters provides a further indication of the future direction of the real estate market: compared to Q2 2019, which recorded 159,792 NTNs, Q2 2023 records a positive change of +15%. This shows that the rise in interest rates, the main reason why real estate buying and selling activity has actually slowed down compared to 2022, is offset by a demand for real estate that still remains high.

Property for sale in Italy with gardens

Italy is known for its beautiful landscapes, and many properties for sale come with gardens of varying sizes and styles. These gardens can range from small courtyards to expansive estates with lush greenery, fruit trees, and even vineyards.

The 5 Italian regions with the fastest rising house prices

The trend in Italian house prices in 2024 and 2025 confirms a clear pattern: the North is driving growth, while Central and Southern Italy show more moderate expansion, with some regions even experiencing a decline.

Buying a home in Italy costs 16% more in 2025 compared to 2019

Buying a home in Italy is becoming increasingly expensive. Compared to 2019, the average cost of purchasing a property has risen by 16%. Milan remains the most expensive city per square metre, while Trieste has recorded the sharpest increases. According to a study conducted by the Centre for Training and Research on Consumer Issues (C.R.C.) in collaboration with Assoutenti, an average worker now needs 11.6 years of salary to buy a home, a clerk requires 9.7 years, while a manager needs only four

From London to Mussomeli for a 1 euro house: "I'll never have a mortgage again"

George Laing is a 30-year-old Englishman who took part in Italy's 1 euro house project by purchasing a property in Mussomeli, in the heart of Sicily. From there, a great adventure began, as he is carrying out the renovation himself, "watching videos on YouTube." This has gained him significant popularity on Instagram, to the point that he will soon appear on one of the UK's main television channels for a property-themed series.

Why one in four Italians wants to move house

According to the RE/MAX European Housing Trend Report 2024, the lack of balconies and gardens, combined with rising energy costs, is fuelling housing dissatisfaction in Italy and across Europe. In line with the European average, 24% of Italians want to move home. Among them, 17% plan to relocate within a year, while 28% are considering moving abroad to improve their financial situation.

Cheap houses for sale in Italy by the sea

Waking up each morning to breathtaking views of the Italian coastline feels like a dream come true. Italy is home to some of the world's most stunning coastal landscapes, stretching from Liguria to Puglia and encompassing the spectacular islands of Sicily and Sardinia. Despite the current economic climate with rising house prices in 2025, now is still an excellent time to explore cheap seaside properties in Italy, with many hidden gems available. Given Italy’s vast coastline, it’s no surpris

The best mountain towns to live in Sicily

Sicily is not just about the sea and beaches: there are many mountain areas full of charm and tradition that offer a peaceful and authentic lifestyle. Living in the mountains in Sicily means enjoying breathtaking landscapes, fresh air, and a slower pace of life, far from the chaos of the cities. Today we're taking a look at 5 of the villages to consider when looking for a home, along with their unique features. These are the best mountain towns to live in Sicily.